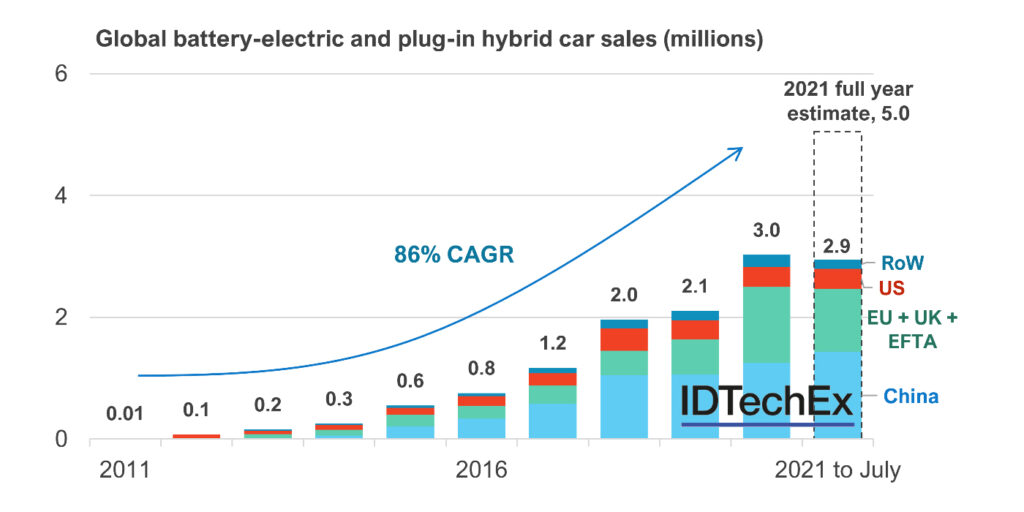

According to new research by IDTechEx, with cars alone, annual EV sales are on pace to surpass 5 million-strong this year, with ~3.5 million battery-electric vehicles (BEV). If they do, it will mean an astonishing growth rate of ~86% CAGR since 2011.

For perspective, IDTechEx has been writing about electric vehicles for two decades, and back in one of its 2011 reports, the group predicted 1.5 million battery-electric car sales by 2021 – an underestimate by over half.

For the last 10 years, electric car markets have been growing rapidly. 2019 is perhaps the exception, with sales dampened by a policy transition in China and lackluster governmental support in the U.S. (ironically, Tesla and GM sold too many EVs and lost federal tax credit eligibility). But in 2021, the momentum behind electric vehicle markets is greater than ever, and strong growth is present in all three top auto markets: China, the U.S., and Europe.

Over the past couple of years, global electric vehicle market growth has been underpinned by Europe, driven by new emissions targets (95g of CO2 per KM). Essentially, these targets make it impossible for automakers not to sell electrified vehicles without avoiding large fines.

In the U.S., Biden has committed $174 billion into supporting electric vehicle uptake (from charging infrastructure to topping up the federal tax credit) and is proposing a new target for 50% electrification by 2030. Sure, this is behind countries like Norway (100% by 2025) or the UK (100% by 2030), but the U.S. auto market is much larger. In terms of the volume of vehicles, this represents one of the largest official commitments by an individual country.

And, in China, purchase subsidy schemes that have been around for over half a decade are being extended to help break in the new energy vehicle double-credit schemes moving forward.

Overall, the net effect of electric vehicle policy from around the world is pushing electric vehicles into the mainstream this decade, creating tremendous opportunities for those operating in the electric vehicle supply chain, IDTechEx says.

While Tesla still leads market share in Europe and the U.S., incumbent automakers have been increasing their skin in the game. This year alone, there have been over 20 announcements related to increasing targets and electrification plans. Tesla’s target is characteristically bullish – 20 million by 2030 with two-thirds global market share. But, as IDTechEx has said before, the company achieves remarkable things on the way to missing its targets.

As the market becomes crowded, range will be a key area on how automakers compete for their slice of the pie.

It is often batteries that take the technology headlines – for good reason – but inverters and motors are very important areas too, where efficiency and weight improvements also improve vehicle range.

Batteries have ~20-30% of the overall vehicle price today, but as their costs fall, the value-add of other components is increasing. Technological innovations in inverters and motors, such as the shift to silicon carbide MOSFETs and high voltage platforms (over 800V), have an important part to play in price parity and product differentiation as the market matures, IDTechEx says, with the potential to increase WLTP range by up to 10% without touching the battery, as well as enabling ultra-fast 350kW DC fast charging.

Here comes hydrogen?

At the other end of the EV spectrum are large, long-haul heavy-duty trucks (HDT). Truck OEMs are under growing pressure to reduce emissions, as one of the largest on-road contributors to them.

While we continue to wait on the highly anticipated Tesla Semi (whose launch has now been further delayed until 2022), the work of OEMs such as Daimler, Volvo and Scania continues to move on at pace. Unlike cars, serious concerns have been raised about the feasibility of deploying battery-electric trucks, especially in long-haul applications, as the energy density of current lithium-ion batteries becomes a limiting factor. However, this challenge is promoting the development of fuel cell technologies that offer OEMs an avenue to a greater range in heavy-duty applications, while (in some scenarios) still achieving low or zero emissions, IDTechEx says.

Using hydrogen as fuel, fuel cells generate electricity on-board a vehicle, providing the primary power source to drive the electric traction motors, or alternatively, acting as a range extender that charges the traction battery during operation.

But, fuel cells are not a silver bullet for heavy-duty transport: Significant hurdles need to be overcome for them to become viable. Aside from the typical technical and economic challenges that accompany any new automotive technology, critical to the success of fuel cell vehicles will be the rollout of hydrogen refueling infrastructure and the production of cheap “green” hydrogen – low carbon hydrogen made from renewable electricity and water, IDTechEx says.

This is not currently taking place. A vast majority of the world’s hydrogen is derived from fossil fuels (so-called “grey hydrogen”) and has a carbon footprint which, considering the intended goal is to reduce emissions from the transport sector, means grey hydrogen makes little sense as a transport fuel.

Nonetheless, today Hyundai is leading the way in fuel cell truck deployment, IDTechEx says, with 46 of its XCIENT fuel cell trucks operating in Switzerland as part of plans to introduce 1,600 FC-trucks by 2025. Hyundai have also announced future FC-truck deployments in the U.S. and China. Toyota, Hino Motors, Daimler, Volvo and Kenworth, along with start-ups Nikola and HYZON, are also investing heavily in this space, the group says.